Private credit has experienced remarkable growth, with assets under management surpassing $2.5 trillion. This expansion is driven by factors such as low interest rates, stringent banking regulations, and inefficiencies in traditional banking sectors. However, concerns about risk-taking behavior, regulatory gaps, and economic vulnerabilities are becoming more pronounced. The sector has expanded into emerging markets, particularly in the Gulf Cooperation Council (GCC), where financial hubs like Bahrain and the United Arab Emirates (UAE) are becoming hotspots for private credit deployment. This blog integrates insights from recent studies, including the BIS Quarterly Review, IMF Global Financial Stability Report, and other industry sources, to examine the global rise of private credit and its broader economic implications.

The Rapid Expansion of Private Credit

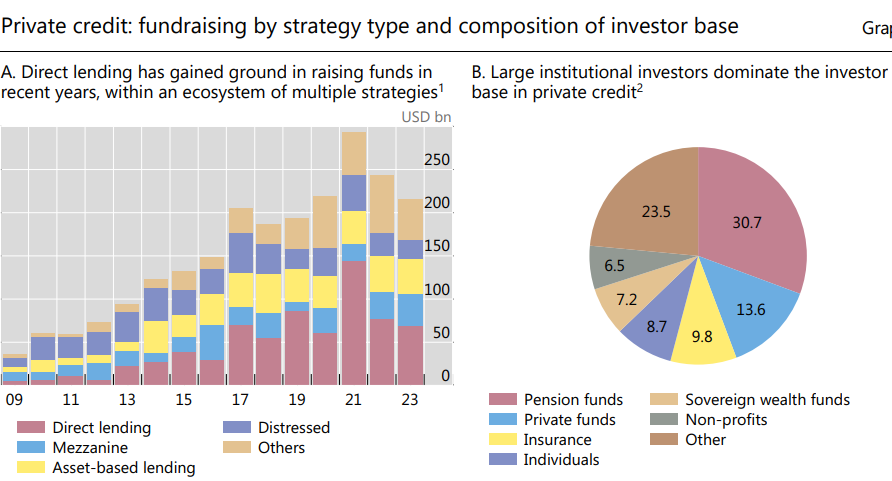

Private credit has transformed into a dominant force in global finance, redefining corporate lending by bypassing traditional banking channels. Over the past two decades, assets under management in private credit funds have ballooned from a modest $0.2 billion to over $2.5 trillion. Unlike traditional bank lending, private credit funds operate with greater flexibility, catering to borrowers who struggle to secure loans from regulated financial institutions.

A significant driver of this expansion is the shifting cost of capital dynamics between banks and private credit investment vehicles. Business development companies (BDCs), a critical part of the private credit ecosystem, have significantly reduced their cost of funding relative to banks. This shift is largely due to declining costs of equity for BDCs and an increase in their leverage, making them a more attractive financing alternative for companies, especially small and mid-sized enterprises (SMEs). However, this rapid growth is accompanied by potential vulnerabilities, including excessive leverage, regulatory blind spots, and a lack of transparency regarding credit quality and risk exposure (IMF, 2024).

Challenges and Risks: A More Opaque Market

Despite the economic benefits private credit provides, the migration of credit from regulated banks and transparent public markets into the more opaque private credit space raises financial stability concerns. The IMF Global Financial Stability Report (2024) highlights the potential for vulnerabilities, particularly in times of economic stress. Unlike traditional bank loans, private credit deals often lack standardized terms and are less regulated.

Another major concern is the trend toward weaker underwriting standards. As competition intensifies, lenders may relax due diligence processes, reducing credit quality and increasing the likelihood of financial distress. The BIS Quarterly Review (2021) notes that private markets, including private credit, are just as procyclical as public markets. This procyclicality means that capital deployment tends to rise in good times but contract sharply in economic downturns, exacerbating market volatility. Given these risks, regulatory bodies are advocating for increased reporting requirements and stronger oversight mechanisms.

Private Credit in Emerging Markets: A Boon or a Risk?

The rapid growth of private credit is not limited to developed economies; emerging markets are also seeing increased activity. Many EMs struggle with less efficient banking systems and limited financial inclusion, making private credit an attractive alternative for businesses that might otherwise lack access to capital. However, this trend also introduces new risks. The IMF (2024) identifies several concerns, including the concentration of lending in high-risk borrowers, potential liquidity mismatches, and the lack of comprehensive regulatory frameworks to oversee the sector.

Private credit’s expansion into emerging markets also raises concerns about capital flight and economic volatility. Many private credit funds operate with foreign capital, which could lead to sudden outflows in times of financial distress. The BIS (2021) notes that private credit funds in emerging markets have shown a strong correlation with stock market performance, meaning they may amplify economic cycles rather than stabilize them. This characteristic makes regulatory oversight crucial in mitigating systemic risks.

Private Credit: A Promising Future in the GCC

The Gulf Cooperation Council (GCC) region is becoming an important hub for private credit. Historically dominated by traditional banking institutions, the GCC’s financial landscape is evolving as private credit giants establish a foothold. Bahrain, home to major financial institutions like Investcorp and Gulf International Bank, has positioned itself strongly in alternative investments, including private credit. The country’s strong regulatory framework and integration with Islamic finance make it an attractive destination for institutional investors seeking Sharia-compliant credit solutions.

In the UAE, major asset managers such as Nuveen and Fortress Investment Group have expanded operations, reflecting the region’s growing significance in global private credit markets. Private credit is filling a crucial gap in the GCC, providing much-needed capital to SMEs that struggle with traditional financing constraints. Moreover, economic diversification efforts in the region are creating demand for new financing solutions, further driving the expansion of private credit.

However, challenges remain. The IMF (2024) warns that the lack of detailed data on private credit exposures in the region makes it difficult to assess potential financial stability risks. Additionally, ensuring transparency and regulatory oversight will be key to maintaining investor confidence and preventing systemic vulnerabilities.

Regulatory Implications and the Road Ahead

The rise of private credit has prompted calls for stronger regulatory oversight. Unlike traditional banks, which operate under strict capital requirements and risk management frameworks, private credit funds often operate in a regulatory gray area. The IMF (2024) recommends that authorities take a more proactive approach, including enhancing reporting requirements, closing data gaps, and strengthening cross-border regulatory cooperation.

Another pressing concern is liquidity risk. Private credit funds typically rely on long-term capital commitments, but the growth of semiliquid investment vehicles increases the potential for redemption risks. Regulators may need to implement stricter liquidity buffers and redemption restrictions to prevent sudden capital withdrawals that could destabilize the market.

The interconnectedness of private credit with other financial institutions also requires closer monitoring. Pension funds and insurance companies have increased their exposure to private credit, and a major downturn in the sector could have spillover effects on broader financial markets. Policymakers must balance fostering innovation in private credit while ensuring that financial stability is not compromised.

As per Avalos, Fernando, Sebastian Doerr, and Gabor Pinter. “The Global Drivers of Private Credit.” BIS Quarterly Review, March 2025, several key regulatory considerations are emerging:

- Transparency and Reporting: Regulators are pushing for enhanced disclosure requirements to ensure that private credit funds provide greater transparency regarding their loan portfolios, risk exposures, and investor structures.

- Liquidity Management: Given the illiquid nature of private credit investments, regulators may impose stricter liquidity buffers or redemption restrictions to prevent sudden capital withdrawals that could destabilize funds.

- Leverage Constraints: With BDCs and private credit funds increasing their use of leverage, authorities are considering potential limits on debt-to-equity ratios to mitigate financial stability risks.

- Investor Protection: As private credit expands beyond institutional investors to retail participants, regulators are exploring measures to enhance investor education and prevent mis-selling of complex credit products.

Conclusion: Navigating Growth with Caution

The rise of private credit represents a fundamental shift in global financial intermediation. While it offers significant benefits by increasing access to capital for businesses and reducing reliance on traditional banking, its rapid growth also necessitates a closer regulatory lens. Emerging markets, particularly in the GCC, are becoming key players in this space, but ensuring financial stability will require careful oversight.

Industry voices and regulatory bodies emphasize the importance of maintaining underwriting discipline and transparency. The GCC is poised to benefit significantly from private credit, and regulatory frameworks must evolve to manage the associated risks. As policymakers and regulators adapt to this changing landscape, striking the right balance between fostering innovation and ensuring financial stability will be crucial. The future of private credit will be shaped not only by market forces but also by the regulatory frameworks that emerge to govern this rapidly growing sector.

References

Aramonte, Sirio, and Fernando Avalos. “The Rise of Private Markets.” BIS Quarterly Review, December 2021.

Cortes, Fabio, Mohamed Diaby, Caio Ferreira, Nila Khanolkar, Harrison Samuel Kraus, Benjamin Mosk, Natalia Novikova, Nobuyasu Sugimoto, and Dmitry Yakovlev. “The Rise and Risks of Private Credit.” Global Financial Stability Report, April 2024.

Lillywhite, Imogen. “As Private Credit Giants Take Root in UAE, Deployment in GCC Is ‘Next Evolution.’” Zawya, March 11, 2025.

Avalos, Fernando, Sebastian Doerr, and Gabor Pinter. “The Global Drivers of Private Credit.” BIS Quarterly Review, March 2025.

Leave a Reply