Introduction: The Rise of Neo-Brokers

The financial landscape is rapidly evolving, with neo-brokers emerging as a disruptive force in retail investing. These digital-first platforms, characterized by their online-only presence and technology-driven services, are reshaping how everyday investors access markets. Unlike traditional brokerage firms, neo-brokers operate without physical branches and rely heavily on technology to facilitate seamless trading experiences. Their core appeal lies in low-cost trading, user-friendly mobile applications, and a strong focus on younger, tech-savvy investors who are new to the financial markets. However, while they democratize market access, these platforms also introduce risks, including hidden fees, conflicts of interest, and regulatory challenges.

Who Are These Neo-Brokers?

Neo-brokers distinguish themselves from traditional brokers by prioritizing simplicity and accessibility. They offer commission-free or low-cost trades, intuitive mobile interfaces, and streamlined account opening processes. Unlike full-service brokers, they do not provide personalized investment advice, instead focusing solely on execution. Their target audience often includes younger retail investors, many of whom are introduced to investing through social media and digital influencers. While this model makes investing more accessible, it also raises concerns about whether inexperienced investors fully understand the risks involved.

The Neo-Broker Business Model

Although neo-brokers attract users with low fees, their revenue model is built on various income streams beyond commissions. One primary source of revenue is Payment for Order Flow (PFOF), where brokers earn rebates from routing client orders to specific market makers or exchanges. This practice has been criticized for potentially prioritizing broker profits over obtaining the best possible execution for investors. Other revenue sources include foreign exchange fees, securities lending, and margin lending, which allow clients to borrow funds to trade. Some platforms also offer subscription models, charging fees for premium research tools or market data. Additionally, they generate income by earning interest on uninvested client funds held in cash accounts. While these revenue strategies keep upfront costs low for users, they create potential conflicts of interest that regulators and investors must scrutinize.

Risks and Challenges

Despite their advantages, neo-brokers introduce several risks that can undermine investor outcomes. One major concern is over-trading, as gamified interfaces ( game like rewards and incentives)and promotional incentives encourage frequent transactions, often leading to unnecessary losses due to bid-ask spreads and market volatility. Hidden fees also pose a challenge, with many platforms advertising “zero-commission” trades while generating profits through wider spreads, foreign exchange charges, or indirect costs. Conflicts of interest arise when brokers prioritize revenue-generating practices like PFOF over securing the best execution for their clients. Additionally, operational risks—such as platform outages, delayed dividend payments, and cybersecurity vulnerabilities—can impact investors’ ability to trade effectively. Regulatory inconsistencies across jurisdictions further complicate oversight, as different countries impose varying rules on disclosure requirements, PFOF practices, and investor protections.

Mis-selling and Fraud Concerns in Neo-Brokerage

The rise of neo-brokers has transformed retail investing, but their aggressive marketing tactics and reliance on digital platforms have also introduced significant risks related to mis-selling and fraud. These concerns primarily stem from misleading advertising, the exploitation of inexperienced investors, and inadequate disclosure of costs and risks.

Misleading Marketing and Misrepresentation

Several regulatory bodies have reported cases where neo-brokers engaged in misleading marketing. Some firms have falsely claimed their services were “free” without adequately disclosing hidden fees such as foreign exchange conversion costs, spread markups, or ancillary charges. Others have used terms like “safe” and “secure” in their promotions without clarifying the associated risks.

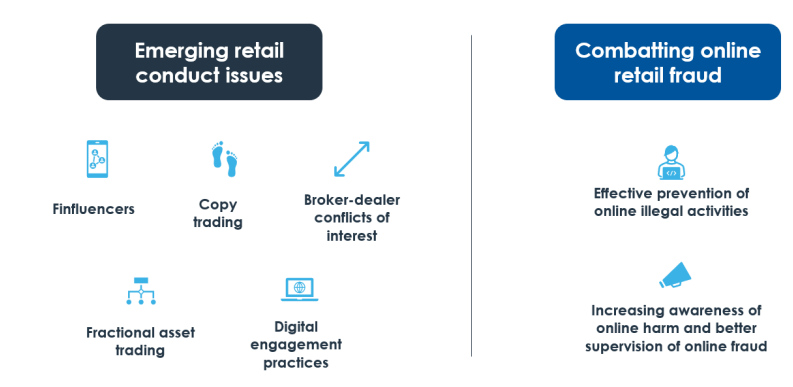

A particularly concerning trend is the use of “finfluencers”—social media personalities paid to promote brokerage services. These individuals often lack financial expertise and may inadvertently misrepresent the risks involved, leading retail investors to make uninformed decisions.

Exploitation of Inexperienced Investors

Neo-brokers primarily target young and novice investors who may not fully understand the complexities of investing. Gamified interfaces, push notifications, and promotional incentives like free shares can encourage impulsive trading behaviors. This can result in excessive trading, which benefits the broker through payment for order flow (PFOF) but often leads to suboptimal financial outcomes for the investor.

In some cases, regulators have taken enforcement actions against firms that marketed complex financial instruments, such as contracts for difference (CFDs) and high-risk crypto assets, to investors without adequately assessing their suitability.

Regulatory Measures

Regulators worldwide are responding to these challenges by imposing stricter rules on transparency and investor protection. Some jurisdictions, including the European Union and Australia, have banned PFOF for domestic equities, while the United States requires brokers to disclose their order-routing practices. In response to concerns about hidden fees, authorities are pushing for clearer disclosures, ensuring retail investors understand the true costs of trading on these platforms. Enforcement actions have also been taken against misleading marketing tactics, with regulators such as Australia’s ASIC and the U.S. FINRA penalizing brokers for deceptive claims and poor order execution practices. Overall, regulators have emphasized:

- Enhanced transparency: Clearer disclosures of fees, conflicts of interest, and product risks.

- Stronger supervision of marketing practices: Restrictions on misleading advertisements and the use of unqualified influencers.

- Investor education: Encouraging awareness of the risks associated with speculative trading and gamification.

- Stricter enforcement: Increased scrutiny on compliance failures, with penalties for brokers found to be engaging in deceptive practices.

As the regulatory landscape evolves, neo-brokers must balance accessibility and innovation with ethical and transparent practices to maintain investor trust. The International Organization of Securities Commissions (IOSCO) has recommended further reforms, including enhanced fee transparency, mandatory investor consent for ancillary services, regular evaluations of PFOF’s impact on execution quality, and robust IT infrastructure to prevent disruptions. These measures aim to create a fairer, more transparent trading environment for retail investors.

The Road Ahead

As the adoption of neo-brokers continues to rise, the road ahead requires a careful balance between fostering innovation and ensuring investor protection. Global coordination will be necessary to harmonize regulations, particularly for cross-border trading platforms. Investor education must also play a central role in helping retail traders understand risks such as over-trading, hidden costs, and conflicts of interest.

While technology has revolutionized market access, regulators and market participants must work together to ensure that this evolution benefits investors rather than exposing them to unnecessary risks. By prioritizing transparency, fairness, and resilience, the industry can create a sustainable ecosystem where both innovation and investor protection coexist.

References

International Organization of Securities Commissions. Consultation Report on Neo-brokers. March 2025. https://www.iosco.org/library/publications/CR022025.pdf.

Annex: Glossary

Neo-brokers – Digital-first brokerage platforms that offer online-only trading services with minimal human interaction, often featuring low fees and mobile accessibility.

Payment for Order Flow (PFOF) – A practice where brokers receive compensation for routing client orders to specific market makers or exchanges, potentially creating conflicts of interest.

Best Execution – A regulatory requirement ensuring that brokers execute client orders at the most favorable terms available, considering factors such as price, speed, and likelihood of execution.

Systematic Internalizers – Entities that execute client orders internally against their own book, commonly used in fractional share trading, which may introduce conflicts of interest.

Conflicts of Interest – Situations where a broker’s financial incentives (e.g., PFOF) may compromise their duty to act in the best interests of their clients.

Retail Investors – Individual, non-professional investors who trade securities for personal accounts rather than for institutional investment purposes.

Maker-Taker Exchanges – Trading venues that offer rebates to liquidity providers (“makers”) while charging fees to liquidity takers (“takers”), influencing order-routing decisions.

Digital Engagement Practices (DEPs) – Technology-driven strategies such as gamification, push notifications, and rewards designed to encourage frequent trading on brokerage platforms.

Leave a Reply